Institutional Insights: Pictet Sales & Trading 'March Seasonality'

March’s seasonality picture is surprisingly constructive for US equities, awkward for bonds, and historically supportive for oil/commodities—with the big caveat that macro/geopolitical shocks are already distorting the “typical” path (especially in crude). Below is an exec-style set of actionable takeaways distilled from the note.

Executive summary

1) US equities: seasonality tailwind, but “path” matters

Base case: March tends to be positive more often than not for the S&P 500 (since 1990: ~+1.0% avg, ~64% positive months).

Key nuance: March 2020 is a major outlier; excluding 2020, March ranks as one of the strongest months in the post-1990 sample (per the note).

Tactical implication: Expect choppier/trend-following behavior early March, with historically healthier performance later in the month.

Action: If adding equity risk, consider staging adds (lighter early March, more willingness to add on dips mid/late-month), rather than “all-in day 1.”

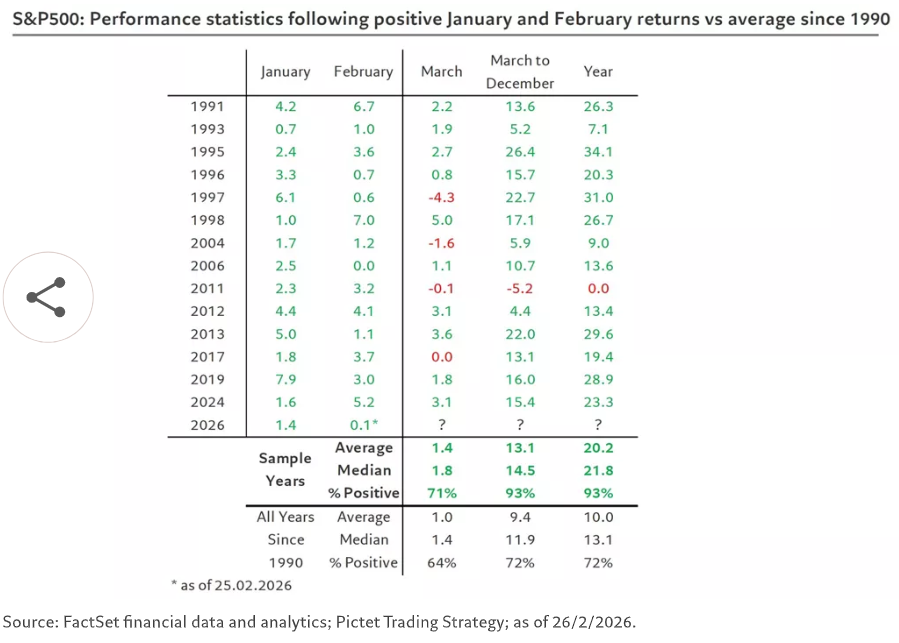

2) “Jan + Feb up” is a bullish conditional signal

In years since 1990 where both January and February were positive, March improved (note cites ~+1.4% avg and ~71% positive occurrences).

Even more important: those years showed a strong March–December follow-through (note cites ~93% positive occurrence and ~+13.1% avg).

Action: Use any early-March weakness as a buy-the-dip framework, with a bias to maintain core equity exposure if the year started positive.

3) Watch the “least favorable” YTD setup: slightly positive YTD into March

If end-Feb YTD is slightly positive (0–+5%), the note shows average March ~0%—i.e., seasonality can flatten despite being broadly positive in other regimes.

Action: Pair equity adds with defined-risk hedges (tight risk limits, collars, or put spreads) if positioning into March is already moderately long.

Sector positioning (US): broad tailwinds, specific tilts

4) Tilt toward Real Estate, Energy, Tech, Consumer Discretionary (seasonal support)

Real Estate: strongest seasonal rebound signal in the note.

Energy / Tech / Consumer Discretionary: strong early-year seasonality that continues through March (note cites March legs around +1.6% Energy, +0.8% Tech, +1.4% Cons Disc on average).

Action: Overweight/lean into these sectors versus market, but prefer liquid expressions (sector ETFs, baskets) if volatility picks up.

5) “Defensives rebound” angle: Utilities & Telecom

Utilities and Telecom historically show rebound characteristics in March.

Action: If you want equity exposure with a calmer profile, use Utilities/Telecom as a partial ballast rather than reducing equities outright.

6) Healthcare: weakest seasonal, but still positive

Healthcare screens weakest on the seasonal lens, though still positive per the note.

Action: Treat Healthcare as neutral/underweight at the margin for seasonal-only trades unless other catalysts dominate.

Other asset classes

7) Bonds: March is historically the toughest month

The note flags March as historically worst month for bonds (proxied by US 10Y futures), within a broader weak window Feb–Apr.

Action: Be cautious adding duration in early March; if you must hold duration, consider tactical hedging (e.g., futures overlay) or favor front-end/less duration-sensitive exposures.

8) Oil & commodities: strongest seasonal window begins (Mar–Jun), but crude already ran

Seasonality supports oil/commodities from March into June.

This year crude is already ~+14% YTD vs typical ~+1% by end-Feb (per note), driven by geopolitical shocks—so the market is ahead of schedule.

Disclaimer: The material provided is for information purposes only and should not be considered as investment advice. The views, information, or opinions expressed in the text belong solely to the author, and not to the author’s employer, organization, committee or other group or individual or company.

Past performance is not indicative of future results.

High Risk Warning: CFDs are complex instruments and come with a high risk of losing money rapidly due to leverage. 71% and 74% of retail investor accounts lose money when trading CFDs with Tickmill UK Ltd and Tickmill Europe Ltd respectively. You should consider whether you understand how CFDs work and whether you can afford to take the high risk of losing your money.

Futures and Options: Trading futures and options on margin carries a high degree of risk and may result in losses exceeding your initial investment. These products are not suitable for all investors. Ensure you fully understand the risks and take appropriate care to manage your risk.

Patrick has been involved in the financial markets for well over a decade as a self-educated professional trader and money manager. Flitting between the roles of market commentator, analyst and mentor, Patrick has improved the technical skills and psychological stance of literally hundreds of traders – coaching them to become savvy market operators!