SP500 LDN TRADING UPDATE 12/3/26

SP500 LDN TRADING UPDATE 12/3/26

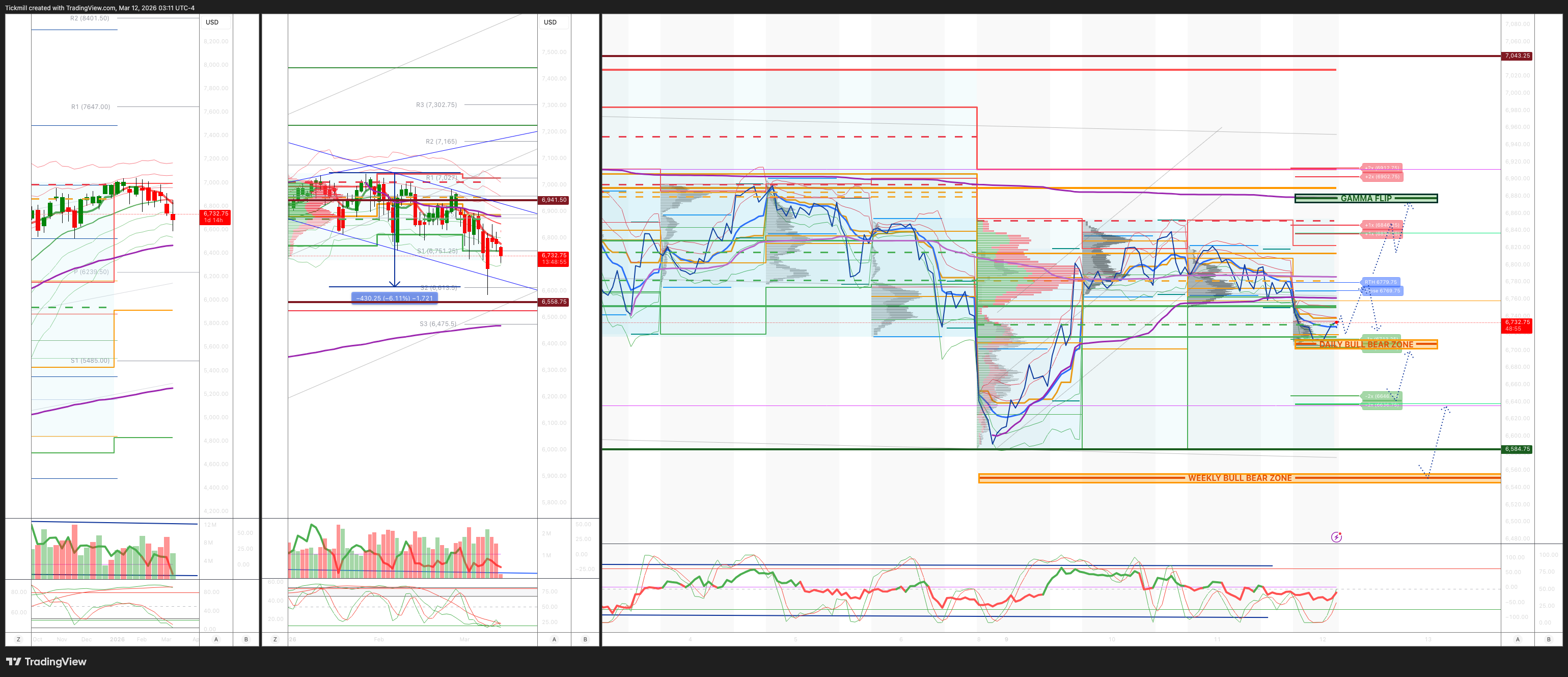

***QUOTING ES1! FOR CASH US500 EQUIVALENT LEVELS, SUBTRACT POINT DIFFERENCE***

WEEKLY BULL BEAR ZONE 6560/50

WEEKLY RANGE RES 6942 SUP 6558

Weekly Straddle Range: 192 -point straddle implies a weekly range of [6558, 942]; monitor 1.5x and 2x moves for key reactions.

March OPEX Straddle: 232.8-point range suggests OPEX-to-OPEX movement between [6677, 7142].

March QOPEX Straddle: 368.55-point range projects [6466, 7203], based on December OPEX.

March EOM Straddle: 255.4-point straddle indicates a monthly range of [6623, 7101]. .

DEC2025 to DEC2026 OPEX straddle spans 945 points, outlining a range of [5889, 7779]."

DAILY VWAP BEARISH 6777

WEEKLY VWAP BEARISH 6868

MONTHLY VWAP BEARISH 6889

DAILY STRUCTURE – BALANCE - 6641/6877

WEEKLY STRUCTURE – OTFD - 6911

MONTHLY STRUCTURE - OTFD

Balance: This refers to a market condition where prices move within a defined range, reflecting uncertainty as participants await further market-generated information. Our approach to balance includes favouring fade trades at the range extremes (highs/lows) while preparing for potential breakout scenarios if the balance shifts.

One-Time Framing Higher (OTFH): This represents a market trend where each successive bar forms a higher low, signalling a strong and consistent upward movement.

One-Time Framing Lower (OTFD): This describ@es a market trend where each successive bar forms a lower high, indicating a pronounced and steady downward movement.

DAILY BULL BEAR ZONE 6710/00

GAMMA FLIP 6882

DAILY RANGE RES 6846 SUP 6713

2 SIGMA RES 6912 SUP 6646

VIX BULL BEAR ZONE 20

PUT/CALL RATIO 1.15 (The numbers reflect options traded during the current session. A put-call ratio below 0.7 is generally considered bullish, and a put-call ratio above 1.0 is generally considered bearish)

TRADES & TARGETS

LONG ON REJECT/RECLAIM OF DAILY BULL BEAR ZONE TARGET RTH CLOSE > DAILY RANGE RES

(I FADE TESTS OF 2 SIGMA LEVELS ESPECIALLY INTO THE FINAL HOUR OF THE NY CASH SESSION AS 90% OF THE TIME WHEN TESTED THE MARKET WILL CLOSE ABOVE OR BELOW THESE LEVELS)

GOLDMAN SACHS TRADING DESK VIEW - ‘Reversal’

S&P closed down 9bps at 6,776 with a Market on Close (MOC) imbalance of $600 million to sell. The Nasdaq 100 (NDX) gained 3bps to finish at 24,965, while the Russell 2000 (R2K) dropped 20bps to 2,543, and the Dow Jones Industrial Average fell 61bps, closing at 47,417. A total of 17.79 billion shares traded across all U.S. equity exchanges, below the year-to-date daily average of 19.65 billion shares. The VIX declined 257bps to 24.29, WTI crude surged 5.75% to $88.23, the U.S. 10-year Treasury yield rose 7bps to 4.22%, gold slipped 26bps to $5,178, the Dollar Index (DXY) increased 41bps to 99.24, and Bitcoin climbed 30bps to $70,462.

Stocks ended slightly lower at the index level as investors grappled with mixed headlines. President Trump suggested a near-term conclusion to tensions with Iran, claiming there’s “practically nothing left to target.” Meanwhile, the International Energy Agency (IEA) announced the release of 400 million barrels of oil, at the high end of expectations. Despite this, oil prices rose over 5%. Additional headlines included the U.S. planning new Section 301 trade probes (NYT) and Iran stating that ending the war requires international guarantees against aggression (BBG). On the macro side, the Consumer Price Index (CPI) was modestly benign but slightly above expectations, with core CPI unrounded at +22bps versus the +20bps consensus. Softer Owner's Equivalent Rent (OER) and rent components were offset by strength in apparel and medical care services.

Momentum factors continued to improve, with our basket rising for a third consecutive session, marking the first such streak since mid-January. Gains were driven more by underperformance in the short leg of the pair. In other areas, alternative assets and private credit names (e.g., OWL -5%, BX -3%, APO -3%) extended declines amid negative sentiment stemming from JP Morgan tightening lending to private credit and marking down certain software loans in its portfolio. This weighed on the broader software sector (excluding ORCL). Our Software vs. Semiconductors pair (GSPUSOSE Index) fell for the third straight session as concerns lingered over software fundamentals, with short-side re-grossing persisting for a second day.

Questions arose about today’s backup in rates, as the U.S. 10-year yield climbed 7bps to 4.23%. The ongoing war has acted as a financial conditions tightener, driving a selloff across the U.S. yield curve and strengthening the dollar due to inflationary pressures from higher commodity prices. Entering the conflict, traders were long 2-year and 5-year Treasuries, expecting rate cuts, but recent volatility has prompted some to double down on these positions. Despite the rate moves, yesterday marked the largest single-day issuance in the investment-grade credit market, with $65.75 billion across 11 deals, led by Amazon’s $37 billion bond offering.

Trading activity on our floor was moderate, scoring a 4 on a 1-10 scale. The floor ended +244bps net to buy, compared to a 30-day average of +70bps. Asset managers were net buyers by $3 billion, with demand spanning sectors such as Technology, Financials, Materials, and Consumer Discretionary. Hedge funds were balanced, with buying concentrated in Healthcare and Utilities, offset by selling in Communication Services. Overall, single-stock trading activity remained muted.

In derivatives, it was a steady day for the volatility desk. Short-dated skew remained steep, with both spot and implied volatility declining. The VIX futures curve remains inverted at the front end, though some easing was observed last night and earlier today. Tomorrow's straddle is pricing in a 90bps move, with the market hovering near the long dealer gamma node. A key challenge remains the market losing more on long gamma than it gains on short skew. This week has seen a shift from hedge reloading to forward volatility buying across asset classes. The desk has observed positioning for a potential violent short squeeze. At current levels, QQQ appears to offer relatively cheap volatility exposure.

Disclaimer: The material provided is for information purposes only and should not be considered as investment advice. The views, information, or opinions expressed in the text belong solely to the author, and not to the author’s employer, organization, committee or other group or individual or company.

Past performance is not indicative of future results.

High Risk Warning: CFDs are complex instruments and come with a high risk of losing money rapidly due to leverage. 71% and 74% of retail investor accounts lose money when trading CFDs with Tickmill UK Ltd and Tickmill Europe Ltd respectively. You should consider whether you understand how CFDs work and whether you can afford to take the high risk of losing your money.

Futures and Options: Trading futures and options on margin carries a high degree of risk and may result in losses exceeding your initial investment. These products are not suitable for all investors. Ensure you fully understand the risks and take appropriate care to manage your risk.

Patrick has been involved in the financial markets for well over a decade as a self-educated professional trader and money manager. Flitting between the roles of market commentator, analyst and mentor, Patrick has improved the technical skills and psychological stance of literally hundreds of traders – coaching them to become savvy market operators!