Finish Line: June 29 — Burnham Calms Gilts, But Weak Mortgage Data Hits Domestic Risk

Finish Line: June 29 — Burnham Calms Gilts, But Weak Mortgage Data Hits Domestic Risk

London hugged the flatline on Monday as investors gave a composed response to Andy Burnham’s economic address but remained cautious ahead of renewed U.S.-Iran talks and a busy week for global central banks. The FTSE 100 was essentially flat in afternoon trading, reversing an initial marginal gain as losses in housebuilders, miners, defence and consumer cyclicals outweighed pockets of strength in technology, financials and telecoms. The most important market signal came from the reaction to Burnham. His speech did not trigger the kind of gilt-market stress investors had feared. Instead, sterling edged higher during the address, with the pound rising to about $1.323, while 10-year gilt yields dipped slightly before stabilising. That response suggests investors were reassured, at least temporarily, by his commitment to fiscal discipline and adherence to the existing fiscal framework. For markets, the message was simple: Burnham sounded more orthodox than disruptive. His emphasis on regional investment, private capital partnerships and working within the rules was welcomed by parts of the business community, including private equity groups such as UK Private Capital. The City of London Corporation also struck a constructive tone, acknowledging his focus on regional development while reminding policymakers that London remains the UK’s core financial engine. But reassurance is not the same as resolution. Think tanks such as the TaxPayers’ Alliance warned that the speech lacked detail on taxation and welfare spending, raising concerns that the fiscal arithmetic may still point toward higher taxes. Investors appear willing to give Burnham the benefit of the doubt, but they still need specifics: who becomes Chancellor, how the Autumn Budget is framed, whether welfare costs are contained, and how infrastructure ambitions are financed. That is why the calm in gilts mattered so much. Over recent sessions, the key UK risk has not been leadership change itself, but whether a new government could boost investment while keeping borrowing credibility intact. Monday’s modest decline in yields suggests Burnham passed the first market test. The harder test comes when rhetoric turns into fiscal numbers.

Domestic economic data were less supportive. Bank of England figures showed net mortgage approvals fell to 56,205 in May, down from a revised 66,034 in April and below expectations of 62,900. That was the lowest level since December 2023. Net mortgage borrowing also fell to £2.9 billion, from £4.4 billion in April and below forecasts of £4.6 billion, marking the lowest level since May 2025 and well below the six-month average of £5.1 billion.That was a clear negative for housebuilders and housing-linked domestic names. Barratt Redrow, Persimmon, Land Securities and Kingfisher all fell, with several names down between 1% and 1.7%. The mortgage data confirm that high borrowing costs are still biting and that the housing recovery remains fragile. Even if Burnham reassures the gilt market, rate-sensitive equities still need actual credit conditions to improve. The geopolitical backdrop also kept risk appetite contained. Investors looked ahead to a fresh round of U.S.-Iran negotiations in Doha on Tuesday, after both sides agreed to halt military strikes and resume talks over shipping routes and transit fees. The easing of direct hostilities has helped markets, but the situation remains unstable. Hezbollah’s leader separately denounced the Israel-Lebanon framework agreement as null and void and warned its implementation could trigger civil war, keeping Middle East risk alive.

The sector picture was mixed. Lion Finance climbed 2.75%, while Computacenter, ICG, Scottish Mortgage, Convatec, Entain, IG Group and Games Workshop gained between 1% and 2%. That pointed to selective interest in financials, growth and quality names, helped by calmer gilts and a modestly firmer pound. BT Group rose 0.7% after signing an agreement to combine its international business in a new joint venture with Verizon. The move was not enough to transform the index mood, but it added to the recent theme of corporate restructuring and strategic action across UK-listed companies. Other gainers included Tesco, Standard Chartered, Coca-Cola HBC, Informa, Shell, Experian, Burberry, Sage, Pearson and Abrdn, which posted moderate advances. The gains were broad enough to prevent a sharper index decline but not strong enough to offset weakness in miners, defence, staples and housing.On the downside, Babcock International dropped about 4.7%, making it one of the day’s heaviest fallers. Endeavour Mining lost 3.7% and Fresnillo fell about 2.3%, as miners came under pressure. British American Tobacco lost 2%, while IAG, Smiths Group, Melrose, BAE Systems, Anglo American, Imperial Brands, Unilever, Antofagasta and Kingfisher shed between 1% and 1.7%.The weakness in miners reflected a combination of caution before the U.S.-Iran talks, a firmer pound, and continuing uncertainty around global demand. Defence names also softened after a strong run, with investors reassessing geopolitical risk premia as negotiations restart. Central banks remain the other major focus. Investors are watching the Sintra Forum, the European Central Bank’s annual policy gathering, for signals on inflation persistence, growth risks and the timing of future rate moves. For the UK, the question is still whether the Bank of England can stay patient while mortgage activity weakens, or whether inflation expectations and geopolitical risks force a more hawkish stance.

Finish Line: The FTSE 100 ended flat as weak mortgage data and caution ahead of U.S.-Iran talks outweighed a calm market response to Andy Burnham’s economic address. Sterling firmed and gilt yields eased slightly, suggesting investors were reassured by his fiscal discipline message. But housebuilders and property names slipped after mortgage approvals hit their lowest level since December 2023. Burnham passed the first credibility test; the next one will be harder – turning pro-growth language into a budget that does not disturb the gilt market.

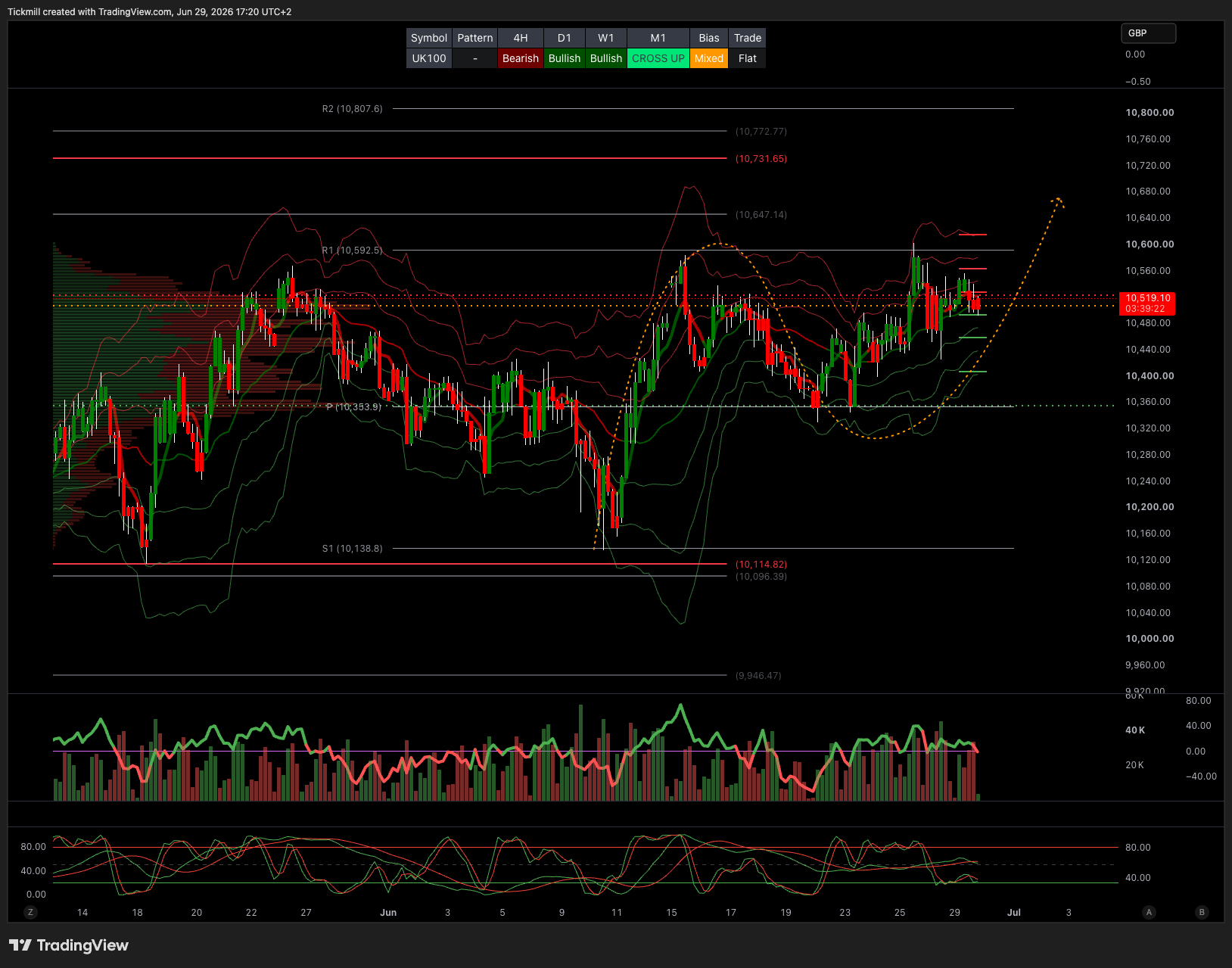

TECHNICAL & TRADE VIEW – FTSE100

Daily VWAP Bullish

Weekly VWAP Bullish

Above 10350 Target 11000

Below 10100 Target 9469

Disclaimer: The material provided is for information purposes only and should not be considered as investment advice. The views, information, or opinions expressed in the text belong solely to the author, and not to the author’s employer, organization, committee or other group or individual or company.

Past performance is not indicative of future results.

High Risk Warning: CFDs are complex instruments and come with a high risk of losing money rapidly due to leverage. 71% and 74% of retail investor accounts lose money when trading CFDs with Tickmill UK Ltd and Tickmill Europe Ltd respectively. You should consider whether you understand how CFDs work and whether you can afford to take the high risk of losing your money.

Futures and Options: Trading futures and options on margin carries a high degree of risk and may result in losses exceeding your initial investment. These products are not suitable for all investors. Ensure you fully understand the risks and take appropriate care to manage your risk.

Patrick has been involved in the financial markets for well over a decade as a self-educated professional trader and money manager. Flitting between the roles of market commentator, analyst and mentor, Patrick has improved the technical skills and psychological stance of literally hundreds of traders – coaching them to become savvy market operators!